Finance

Basic Investing Finance for Dummies (Me)

Some general notes about financial investing for my personal reference. Not intended to be advice for anyone, not even dummies. Accurate to the best of my knowledge for 2022. Consult a financial professional before making any decisions regarding your personal finances.

Most reference links are Charles Schwab & Investopedia which I find informative & concise without annoying popups. I am not affiliated with the reference links other than having a Schwab account. The Amazon/Audible books are affiliate links.

Page 1: Overview

Page 2: Read More

Page 3: Books & Video

Page 4: Glossary of Terms

Page 5: Resources & Quotes

3 Simple Steps

- Contribute at least enough to maximize 401k Employer Match to get the “free money“.

- Max out yearly Roth IRA contribution limits because it grows Tax Free!

- Invest excess money to gain a higher rate of return than a savings account and outpace inflation.

Here’s how and why

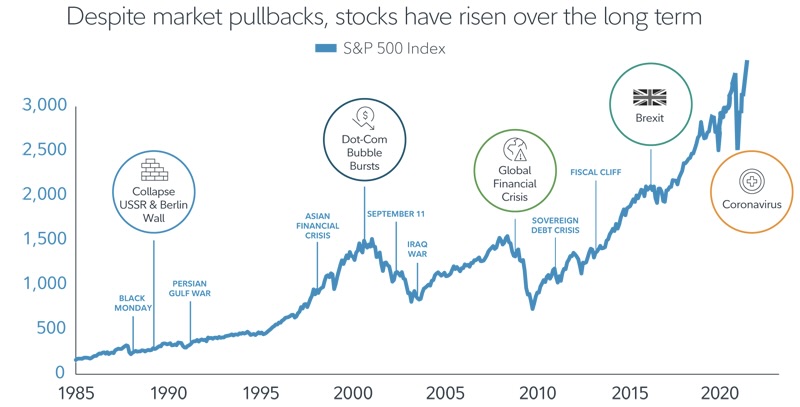

Time in the Market is the single most important factor to long term gains.

So Start Early but it’s never too late so START NOW!

401k

If your company has a 401k and matches, put at least the percent required to max out their matching contribution. It’s free money and not even a dummy passes on free money! Plus you won’t notice much of a difference on your check because it comes out pre-tax.

* Only put more than the matching % if you have already maxed out your Roth IRA which is far more tax advantaged and profitable than a 401k. So just enough to get the free money match.

Read more Page 2

Roth IRA

Max out your yearly Roth IRA contributions ($6K in 2022*). Capital Gains aren’t taxed in a Roth IRA! Whether your Roth earns millions or billions, your gains are tax free. Work overtime if you must to max out your Roth! Invest in safe, reputable low cost Passively Managed (lower fees & taxes) Mutual Funds, Index Funds or EFTs that match or track the components of a financial market Index (IVV, VOO, SPY, SCHB, QQQ etc.) and maybe some established high dividend stocks or ETFs. Roth is so taxed advantaged that to qualify you must fall below an income limit to participate (MAGI must be under $144,000 single, joint $214,000 -tax year 2022). Back door and loop holes exist.

Read more Page 2

Brokerage

Start an individual brokerage account to park some excess money with the goal to earn more than interest in a savings account and outpace inflation. Invest in safe, reputable low cost Passively Managed (lower fees & taxes) Mutual Funds, Index Funds or EFTs that match or track the components of a financial market Index (IVV, VOO, SPY, SCHB, QQQ etc.) and maybe some established high dividend stocks or ETFs.

Read more Page 2

Why Invest?

“Why do you invest?”

“Because I know how math works!”

Compounding is the process in which an asset’s earnings, either from capital gains or interest, are reinvested to generate additional earnings over time.

Investopedia Video: Compound Interest Explained: https://youtu.be/wf91rEGw88Q

The Power of Dividend Investing | The Snowball Effect by Dividend Data: https://youtu.be/vffTJV0IzHM

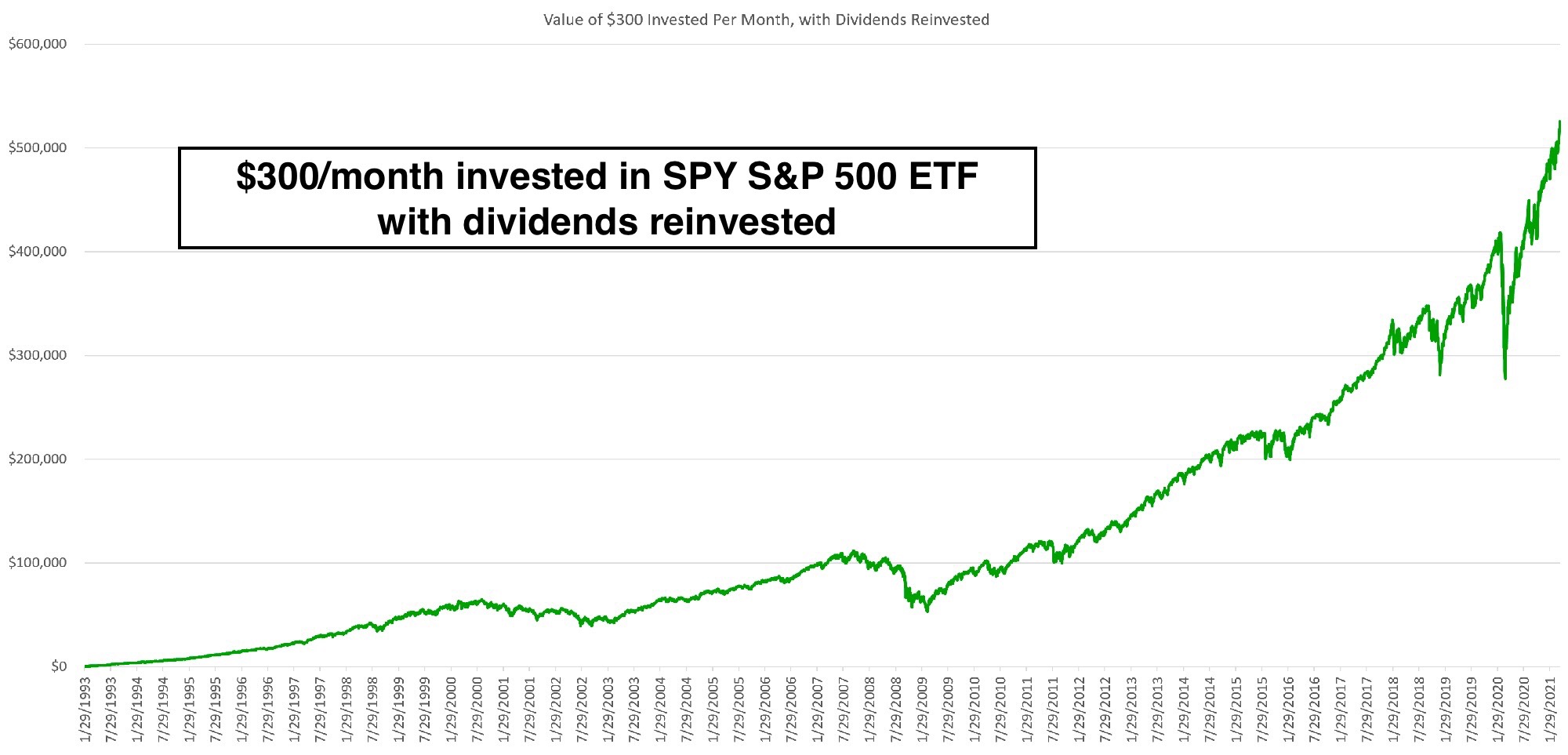

Investing $300 Per Month Into The S&P 500 (HUGE Return): https://youtu.be/ZdShimSogqY

Is Investing Risky?

If you make bad choices or gamble then yes, it is risky.

Don’t do that! I will explain below but…

In the short term investing can be risky but we are not investing for the short term. In the long term however, not really*. Not any more risky than parking your money in the bank loosing to inflation or investing in real-estate etc. The market will recover, if not, you’re screwed anyway no matter what you did with your money. You will need lead and silver. “Ok I get lead for bullets but why silver?” “Vampire and Werewolves duh!”

Read more Page 2

7 investing myths & realities about the stocks: Fidelity article link

I signed up for my 401k at work but I don’t know anything about stocks or the stock market. How do I start a Roth IRA & Brokerage and what do I invest in?

Open an account with a reputable Full Service Broker like:

How to open a Charles Schwab Account Youtube Video

How to open a Vanguard Account Youtube Video

How to open a Fidelity Account Youtube Video

I use Charles Schwab. I first signed up for an Individual Brokerage Account then added the Roth IRA Account but you can start any account first then later add any of the accounts they offer including Retirement, Education, Brokerage, Checking & Savings Accounts.

I’ve opened my Roth IRA & Brokerage, what next?

A Roth or a Tradition IRA are not an investment, they are how an investment is treated for taxes. A Roth IRA is not like your company 401k where your money is withdrawn and invested for you. It’s an Individual Retirement Account in which after tax dollars are invested by you and earnings are tax free. It’s like a regular brokerage investing account but has contribution limits and withdraw age requirements. So you have control over what you invest in but must decide what to invest in.

Read more Page 2

Roth IRA & Brokerage

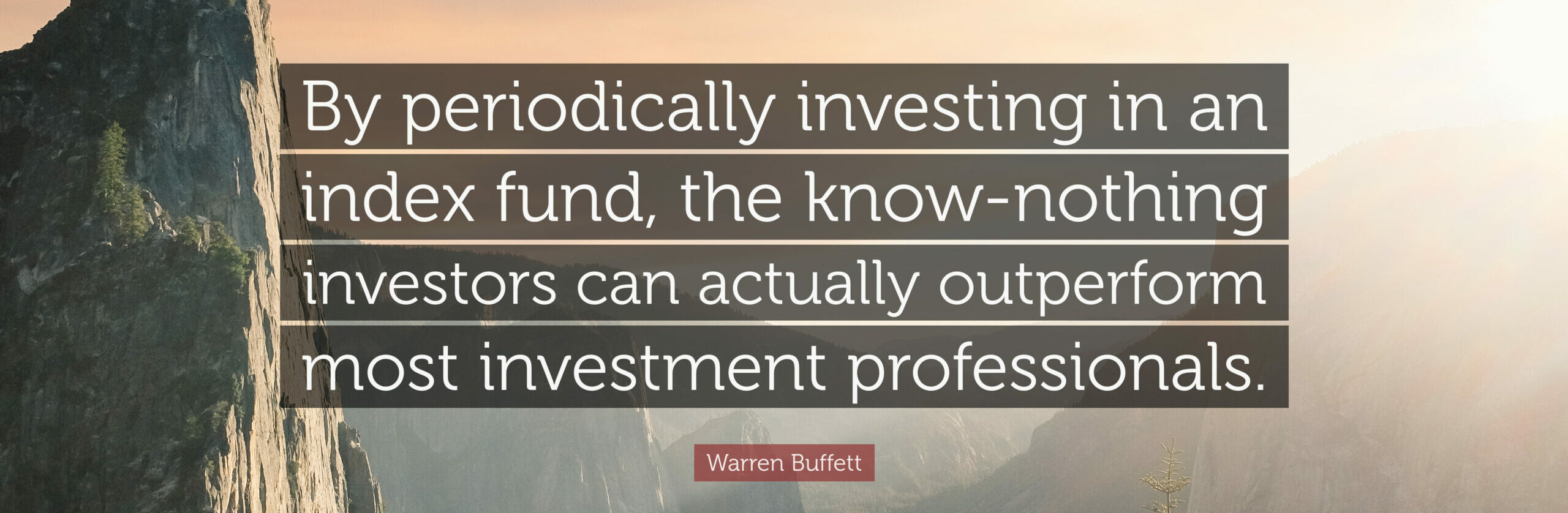

You don’t need to pick stocks or understand the stock market to invest!

Picking stocks is difficult, can be risky and requires continued evaluation.

Even experts struggle and fail.

Instead of picking individual stocks, consider buying low cost index funds and holding onto them. This type of diversified fund typically stays relatively constant & avoids the ups & downs that come with picking single stocks.

Passive investing in index funds has even been shown to be more successful than professionally managed funds.

Actively Managed vs Passively Managed

Read more Page 2

Just buy reputable ETFs that that track an index (like the S&P 500) & select reinvest dividends.

Set it & Forget it, don’t look at them again until close to retirement or withdrawal.

(DRIP) Dividend Reinvestment Plan: read more

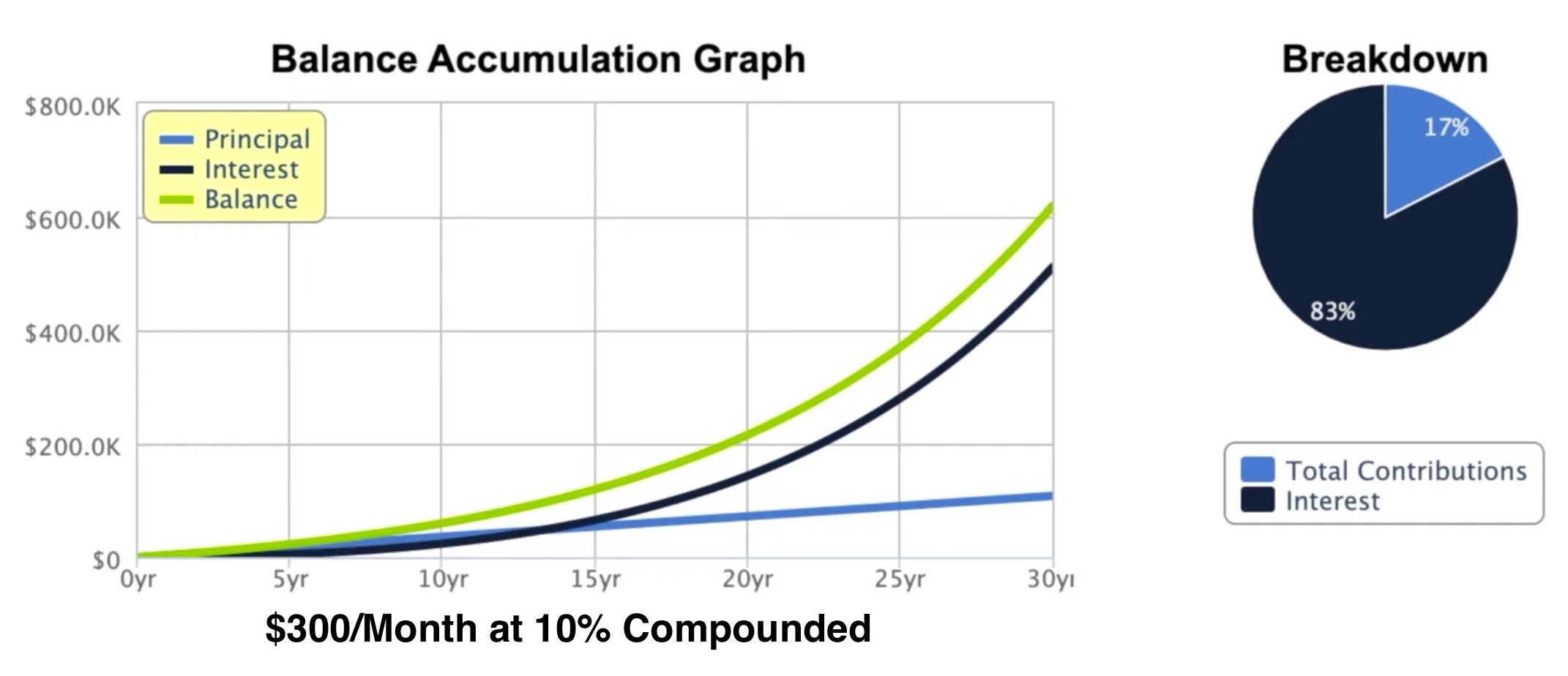

Example Investment:

85% into IVV S&P 500 ETF

15% into QQQ Nasdaq 100 ETF

Some ETF examples:

IVV: iShares Core S&P 500 ETF

VOO: Vanguard S&P 500 ETF

SPY: State Street SPDR S&P 500 ETF

SCHB: Schwab US Broad Market ETF

QQQ: Investco Nasdaq 100 ETF

How much to contribute to Roth and when?

You are only allowed to contribute a limited amount to your Roth IRA annually since gains are tax free. As of 2022 that limit is $6k per year ($7K if 50 or older).

If you haven’t been contributing on a scheduled basis (just started account) and have the lump sum $6K, you can put last years contribution in if you do it before April 15th, this takes priority over the current year due to the time constraint. Just put all $6k for last year or if you nearing the end of this year. We will do Dollar Cost Averaging monthly investments from this point on.

Again, if you have to work overtime to max out your Roth contributions, do it!

That’s $500 a month invested going forward to max out your Roth.

Watch this video if motivation is needed: Investing $500/m in S&P 500

“I can’t afford $500 month” Modify your behavior, eliminate unnecessary expenses, reduce luxury expenses that you can do with less often and invest what you can.

An important note about ROTH IRA that is different than traditional IRA or 401K.

You can withdraw your Roth IRA contributions at any time, for any reason, with no tax or penalties. That’s because your contributions are with after tax money, you’ve already paid tax on the money (withdrawals on earnings work differently)*.

Although it best not to withdraw, it is a little peace of mind knowing the money you contributed can be accessed should a dire emergency require it. No, a sale on a thing does not constitute an emergency.

I was once out of work for 6.5 months due to injury and due to rule structure was not allowed to access funds from my 401k or annuity until after I miss a house payment, yikes! Fortunately that didn’t happen but it was getting close.

Roth IRA Withdrawal rules:

Charles Schwab link

Investopedia link

Read more Page 2

How best to invest on a scheduled basis

“Time in the market beats timing the market”

Dollar Cost Averaging

DCA is an investment strategy in which an investor divides up the total amount to be invested across periodic purchases in an effort to reduce the impact of volatility on the overall purchase. The purchases occur regardless of price and at regular intervals.

-insert chart here-

Dollar Cost Averaging articles:

Charles Schwab link

Investopedia link

Does timing the market work? Charles Schwab link

Dollar Cost Averaging Youtube videos:

What is Dollar Cost Averaging? (Dollar Cost Averaging Explained) YouTube Video

So going forward if we want to max out our Roth IRA contributions, we manually invest or set our account to automatically invest $500 monthly ($6k yearly) into ETFs. Some accounts allow you to buy slices of a stock with the remaining money after whole stocks are purchased (but for no practical reason, I don’t like that idea). I believe reinvested dividends works this way as well but will have to research it.

I am contributing to 401k & Roth IRA, what next?

Ok, we have maxed out our Roth IRA, investing the matching contribution to 401k and because we don’t fall for consumerism, marketing & general over consumption, we have left over money we would like to invest. Yes I like run-on sentences, it’s how my brain works. Out of sequence also, Yoda style, deal with it.

Should I invest more in my 401k or open an individual brokerage account and invest or do both?

Well that depends. Either is a good option as well as both. Depending on the situation one may be better than the other.

So here is some advice for myself and no one else.

-If you need to reduced your taxable income (MAGI) for any reason (qualify for Roth IRA etc.) then increase your contribution to your 401k. Otherwise don’t. You will almost certainly get better returns on low cost ETFs mentioned than your managed 401k. That’s just how the compounding action of fees and expenses of managed funds work. That doesn’t make 401ks a bad thing, they are a good thing, especially the matching free money. Free money at a lower return is better than no money at a higher return. They just may not be the best thing for a given situation.

–If you don’t need to reduce your taxable income, then invest extra money in an individual brokerage account in the index fund ETFs we mentioned prior.

Just remember 401k is withdrawn pretax, and Roth IRA contributions are post tax.

401k is tax-deferred, you pay taxes when you withdraw it.

Roth IRA is tax free, you don’t pay tax when you withdraw it.

Read more Page 2

Now we must learn some basic tax rules for our individual brokerage account (not Roth IRA, it’s tax free)

Realized Gains, Unrealized Gains,

Stock Sales & Capital Gains Tax

If you’re playing around with game like stock apps like Robbing U Hood that use fireworks and other dopamine tricks, franticly clicking the screen buying and selling like collecting coins on a child’s game, you may be in for a big surprise come tax time (and probably damaging your mind in the process). Every profit from sale (Realized Gain) must be accounted for and taxed. Just the time to input this information alone at tax time is encouragement not to buy and sell frivolously. We want to buy and hold.

Realized Gains are those that have been actualized by selling a position for more than you paid. An Unrealized (paper) Gain, is one that has not been realized yet. Realized Gains result in a taxable event, but Unrealized Gains typically do not.

Investopedia article on Realized vs Unrealized Gains

Short Term Capital Gains Tax:

Shares held for a year or less are subject to your income tax rate (much higher than LT-CGT).

Long Term Capital Gains Tax:

Shares held for a year and 1 day or longer are subject to Long Term CGT which is 15% for most people (much lower than ST-CGT).

2022 long-term capital gains tax brackets

| For single filers with taxable income of… | For married joint filers with taxable income of… | …this is the long-term capital gains rate |

|---|---|---|

| $0 to $41,675 | $0 to $83,350 | 0% |

| $41,676 to $459,750 | $83,351 to $517,200 | 15% |

| Over $459,750 | Over $517,200 | 20% |

So it should be very clear at this point that the average investor should avoid Short Term Capital Gains Tax. Leave that bull$#it to the ***cidal day traders and **generate gamblers.

Remember neither applies to your Roth which is why the Roth is so advantaged.

If you have to work overtime to max out your Roth, do it!

Read more Page 2

In Summary

- Contribute at least enough to maximize 401k Employer Match to get the “free money“.

- Max out yearly Roth IRA contribution limits because it grows Tax Free!

- Invest excess money to gain a higher rate of return than a savings account and outpace inflation.

Of course it should go without saying don’t spend more than you make, pay credit card in full each month, have an emergency fund, have appropriate insurances, etc.

Financial Videos

“How The Economic Machine Works by Ray Dalio”

An excellent video explaining how the economy operates.

“How to (Legally) Never Pay Taxes Again”

More realistically, how to reduce your tax burden

Financial Books

The audible & Amazon links are affiliate links in which if you make a purchase I earn very little at no extra cost to you. So if your going to make amazon purchases, do it through one on my links bc I earn a tiny commission on the total order which turns a tiny commission into a small commission which helps pay the internet bill.

Try Audible

The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel read by Chris Hill https://amzn.to/38wWz0M

Rich Dad Poor Dad: What the Rich Teach Their Kids About Money – That the Poor and Middle Class Do Not! By Robert T. Kiyosaki, read by Tim Wheeler https://amzn.to/3nSHuvH

Also subscribe to my Youtube Channel. I have over 20 million views but a measly 20 thousand subscribers! That is one out of wack ratio but you can help fix that by clicking here

You can help support the creation of content, tutorials & projects with a small donation via Paypal and/or by using affiliate links on Shop Pages. Also subscribing to my YouTube Channel helps a ton!

Thanks for your support!

Page 1: Overview

Page 2: Read More

Page 3: Books & Video

Page 4: Glossary of Terms

Page 5: Resources & Quotes