Finance

Page 2: Read More

Page 1: Overview

Page 2: Read More

Page 3: Books & Video

Page 4: Glossary of Terms

Page 5: Resources & Quotes

401k, Roth IRA & Brokerage (continued)

401(k) & Roth IRA Contribution limits for 2022

| Contribution limits 2022 | Under age 50 | Age 50 or older |

| 401(k) | $20,500 | + $6,500 ($27,000) |

| Roth IRA | $6,000 | + $1,000 ($7,000) |

2021-2022 401(k) Contribution Limits: Inv. link

2021-2022 Roth IRA Contribution Limits: CS link

Remember a Roth IRA or a Tradition IRA are not an investment, they are how an investment is treated for taxes.

401k vs Roth IRA which is better?

Well mathematical or psychologically?

Mathematically a Roth IRA invested in low cost ETFs is far superior, duh, that $#it grows tax free and has lower costs which means more profit to compound. It’s not even close unless your company offers a high matching contribution and it still may not be close.

Psychologically a 401k is better for most people because contributing to the market (Time in the Market) is the single most important factor in gains. If your not contributing, you not gaining and more people contribute to a 401k because its easier and automatically withdrawn from your check.

The one you contribute to will always outperform the one you don’t contribute to.

This is why some suggest to contribute to the 401k the amount required to get full matching contributions (free money) and then max out the Roth IRA before contributing any more to the 401k.

If you don’t get any matching contributions to a 401k and investments funds are not sufficient to max out a Roth IRA and contribute to a 401K. In most cases contributing to the Roth IRA is a better option. But realistically you can contribute 5-7% to your 401k without noticeable difference in the take home pay on your check.

The Roth IRA contribution withdraw rules offer some peace of mind as well should an emergency require those funds (like being out of work 6.5 months).

Tax Deferred vs Tax Free which is better?

Pre-Tax Income Tax Deferred Investment (401k) vs Post-Tax Income Investment Tax Free Gains (Roth)

Tax Free and it’s not even close! Duh

The theory that tax deferred is better because we will reduce tax liability while earning at a higher income (higher tax rate), and the money will be withdraw at a lower income tax rate during retirement can be misleading and in many situations is flat out incorrect.

If you have many children and deductibles you may well be at a lower tax rate during your working life than when you retire. If you planned well for Retirement, you will likely be at a higher income which means a higher income tax rate.

Do we know what the tax rate will be in the future?! Will taxes likely go up or down? Someone has to pay for 2008, that spiky ball thing in 2020 and ever increasing government benefits and programs. That person is YOU! The income tax rate will almost certainly be higher in the future.

Would you rather pay tax on $1 today or pay tax on $5 in the future? Or put another way, pay tax on a seed or pay tax on the harvest?

Also keep in mind that the tax rate today is known, the tax rate in the future is unknown.

With these considerations, given the choice, to me Tax Free is better than Tax Deferred.

However Tax Deferred can be a useful addition to Tax Free, for lowering our Modified Gross Income (MAGI) for various reasons including falling into Roth eligibility as discussed previously.

This is often disputed though but that fact that you’re only allowed $6k a year in Roth IRA but allowed over $20k in 401k contributions should tell you something!

Just find a way to do both and don’t stress over it!

How 401(k) Matching Works: Investopedia article link

Reasons to max out your 401(k)

1) – Your income is unusually high and you want to reduce tax liability.

If you will be at an increased income for an extended period of time, for example on an overtime job that lasts for months or even years (yes you, elevator mechanics, electricians, welders, etc). Since the overtime is extra money you aren’t accustomed to, you won’t feel the sting of it being withdrawn. If you don’t increase your contributions you will feel the sting of the taxes withdrawn!

On your hardest worked hours, your overtime hours, you will be taxed at the highest rate. Most people are willing to pay their fair share but if you work 70-80 hour weeks you will be paying far more than your fair share while working yourself to death.

Increasing your 401(k) contributions is one of the simplest ways to reduce tax liability. You may even have to max it out at $20,500. Once the overtime is finished you can lower your contribution to your normal percentage.

2) – Your expenses are unusually low and you have excess money.

You’re young and don’t have a family or many bills yet. This is ideal bc of early start on investing (time in the market) and it helps develop good habits and behavior early.

Or you’re an empty nester now (kids have moved off) and maybe you’ve downsized from a big house to a tiny house or motor home etc. Your bills are now much lower than previously.

If you have a significant excess of money vs bills you may want to max out the 401k along with other investments.

Either case just put it in!

You won’t miss the money and you’d just find a way to piss it away on the needless anyway. Plus you’ll gain a sense of confidence and respect that comes with financial responsibility. It may even drive your stupidvisor nuts out of jealously.

| Weeks Worked | 2022 Annual Contribution Limit (under 50) $20,500 | 2022 Annual Contribution Limit (50 or older) $27,000 |

| 52 | $394.24 / week | $519.23 / week |

| 50 | $410.00 / week | $540 / week |

| 48 | $427.08 / week | $526.50 / week |

Why Invest? (continued)

Charts and graphs to come but check this out in the mean time:

US News & World Reports

9 Charts Showing Why You Should Invest Today

https://money.usnews.com/investing/investing-101/articles/2018-07-23/9-charts-showing-why-you-should-invest-today

Is Investing Risky? (continued)

We first need to differentiate short term risk from long term risk.

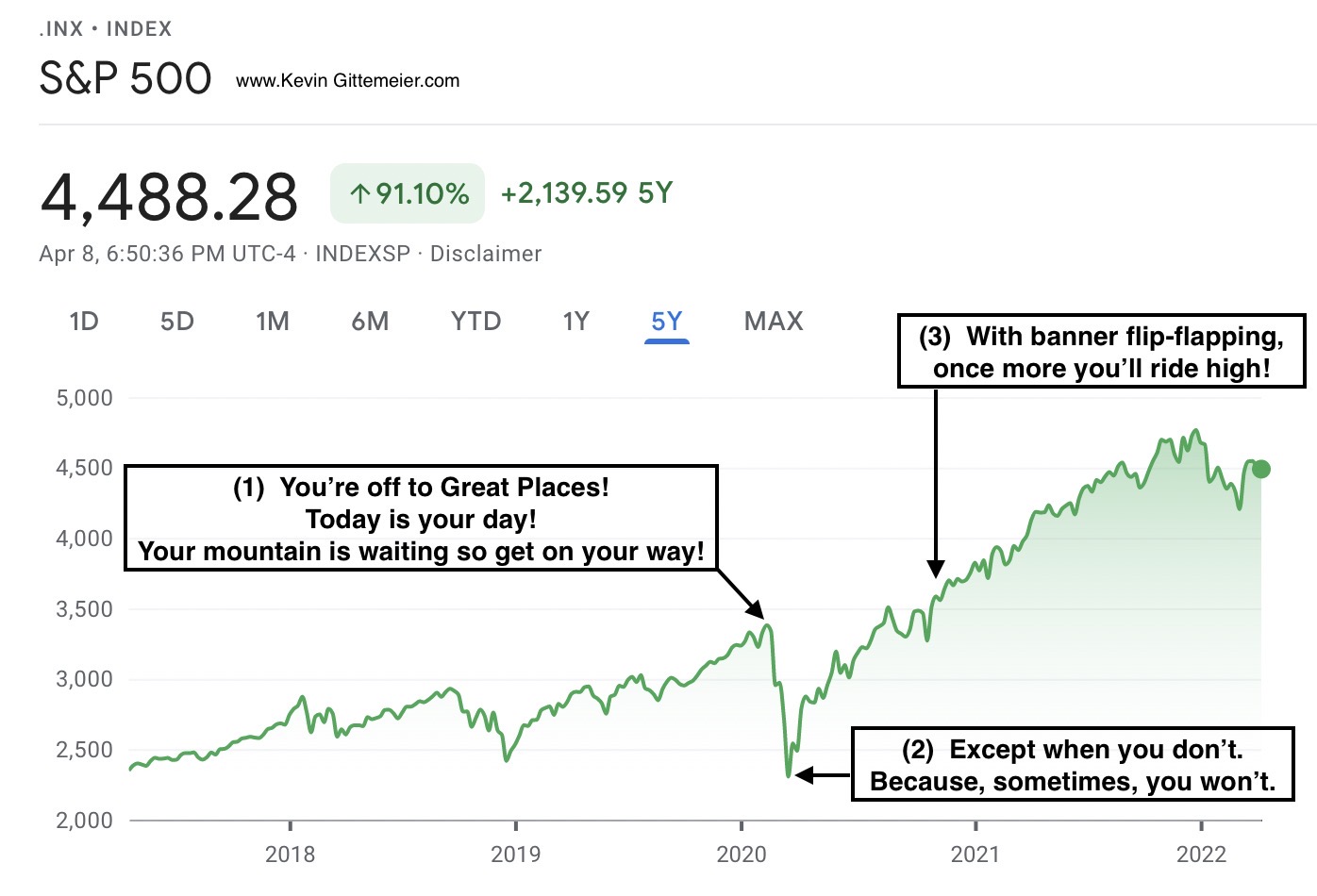

Let’s look a the S&P 500 Index chart below.

Had we invested at the peak just before that spiky ball sea urchin looking thing wrecked the economy in 2020, we might have felt devastated believing we just lost forever most of our money. Sure enough if we cashed out, we did but if we just held our investments, they were back up in less than a year. So unless we absolutely had to have that money, at that time, that enormous loss did not affect us long term.

“The Sea Urchins are on the march!” CJ tried to warn us in 2015.

We didn’t listen, we only laughed.

Had I given it any care, today I would be a millionaire.

So the short term risk doesn’t much affect the long term investor.

Relatively speaking, long term risk is low. If things get so bad that the entire economy is collapsed for decades or longer (longer than the Great Depression) we are likely screwed no matter what we did.

Let us take a moment to remember the sage wisdom from that great book “Oh the Places You’ll Go”

You’re off to Great Places!

Today is your day!

Your mountain is waiting so get on your way!

Wherever you fly, you’ll be the best of the best.

Where you go, you will top the all the rest.

Except when you don’t.

Because, sometimes, you won’t.

With banner flip-flapping,

once more you’ll ride high!

Ready for anything under the sky.

Ready because you’re that kind of guy!

And will you succeed? Yes! You will, indeed! (98 and 3/4 percent guaranteed)

“Widgets have never cost more, let’s go buy a bunch!

Huge sale on widgets lets sell ours now” – said no one.

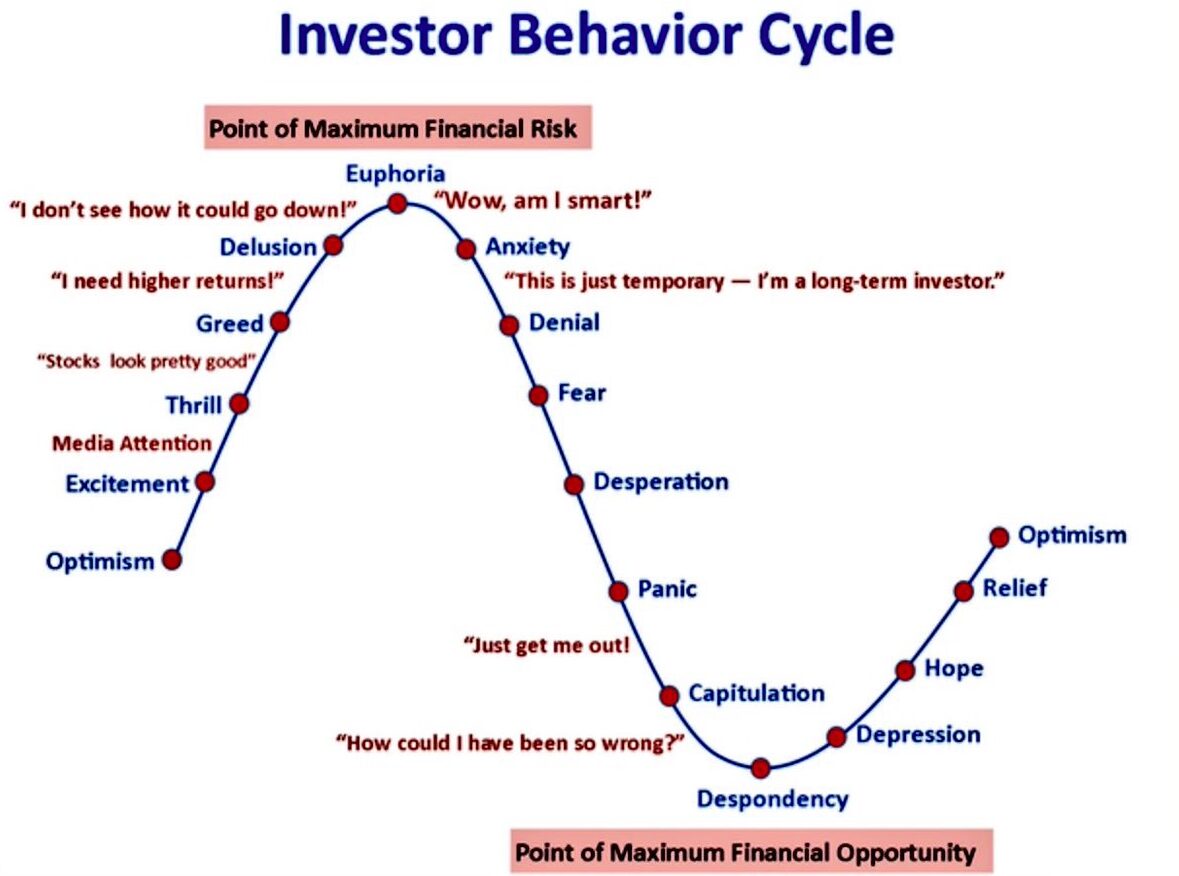

Warren Buffett on Mr Market analogy

“Most people react the wrong way to stock prices… They think the stock market is there to instruct them.

And Mr Market is this partner you have in investing. He is a remarkably obliging parnter.

This guy comes around every day and he tells you what he’ll pay you for your interest in the business or what he’ll sell you more at the same price.

Nobody ever does that in private business….You’d be at a terrible disadvantage.

And you’d be at a particular disadvantage if you’re Mr Market because Mr Market… This guy is an alcoholic manic depressive, he is as unsound as they come… he is going to name all kinds of crazy prices and you don’t have to pay any attention to him except when it’s to your advantage. That’s once a year or once every 5 years, 1 stock out of 3,000.

All you have to do is sit there, you have no moral responsibility to this jerk. He is naming these numbers, you didn’t ask him to but he’s doing it and all you have to do is pick the one time when he is particularly depressed or particularly manic or particularly drunk or whatever it may be.. and you take advantage of him.”

Warren Buffett

I’ve opened my Roth IRA & Brokerage, what next? (continued)

content coming soon

Actively Managed vs Passively Managed

Short bit about this here (tax inefficient, high costs etc.)

Maybe a chart showing active vs passive comparison results over time

Active vs. Passive Investing: What’s the Difference?: Inv. article link

Should I Reinvest Dividends?

Dividend Reinvestment Plan (DRIP) investopedia article link

– A program that allows investors to reinvest their dividends into additional shares or fractional shares of the stock.

If you’re trying to maximize profits over the long term, yes! Especially if these investments are in a Roth where the compounded dividend profits grow tax free.

Dividends purchasing more stock = more dividends which = more stocks purchased and so on.

However many people nearing or in retirement opt to take dividend payouts as a source of income. If you invest early enough and reinvest dividends, by retirement (due to compounding) you’ll be in a better position to utilize dividend payouts as a source of income.

Should You Reinvest Dividends?: Investopdia article link

How to Reinvest Dividends from ETFs: Investopedia article link

How much to contribute to Roth and when? (continued)

As much a possible and on a scheduled basis, DCA Dollar Cost Averaging.

more content coming soon

Roth IRA Contribution Limits by Income (Tax year 2022)

| Single Filers (MAGI) | Married Filing Jointly (MAGI) | Married Filing Separately (MAGI) | Maximum Contribution under age 50 | Maximum Contribution for age 50 and older |

|---|---|---|---|---|

| under $129,000 | under $204,000 | $0 | $6,000 | $7,000 |

| $130,500 | $205,000 | $1,000 | $5,400 | $6,300 |

| $132,000 | $206,000 | $2,000 | $4,800 | $5,600 |

| $133,500 | $207,000 | $3,000 | $4,200 | $4,900 |

| $135,000 | $208,000 | $4,000 | $3,600 | $4,200 |

| $136,500 | $209,000 | $5,000 | $3,000 | $3,500 |

| $138,000 | $210,000 | $6,000 | $2,400 | $2,800 |

| $139,500 | $211,000 | $7,000 | $1,800 | $2,100 |

| $141,000 | $212,000 | $8,000 | $1,200 | $1,400 |

| $142,500 | $213,000 | $9,000 | $600 | $700 |

| $144,000 & over | $214,000 & over | $10,000 & over | $0 | $0 |

2021-2022 Roth IRA Contribution Limits: CS article link

Roth IRA Contribution Rules: A Comprehensive Guide: Inv. article link

I am above the income limit to contribute Roth IRA, what can I do?

Consult a professional! You don’t want to mess this up but here are some general notes to better inform yourself before meeting with a professional:

Roth IRA Income Limits

Eligibility to contribute to a Roth IRA depends on your overall income. The IRS sets income limits that restrict high earners but there are loop holes with back door conversion methods.

Turn Traditional IRA assets to Roth IRA assets through annual conversion.

Roth IRA Conversation Ladder.

- Charles Schwab Roth IRA Conversion article link

- How to Set Up a Backdoor Roth IRA Investopedia article link

- Backdoor Roth IRA – How Does It Work? by Joe Broe YT video

- Roth Conversion Ladder Explained – Can You Retire Early? by Joe Broe YT video

- How Do I Move to a Roth? by Ramsey YT video

- Should I Hold Off On My Back-Door Roth Conversion For This Year? by Ramsey YT video

Roth IRA vs Tradition IRA

Charles Schwab article link

Inherited IRA

Charles Schwab (what is) article link

Charles Schwab (rules) article link

Investopedia article link

Investopedia article link

Roth IRA Contribution Rules: A Comprehensive Guide

Everything you need to know about contributions and distributions

Table of Contents

Roth IRA Income Limits

Roth IRA Contribution Limits

Timing Your Contributions

Tax Breaks for Contributions

Roth IRA Withdrawal Rules

Specials Changes in 2020

Recordkeeping for Contributors

Frequently Asked Questions

The Bottom Line

I am contributing to 401k & Roth IRA, what next? (continued)

content coming soon.

Realized Gains, Unrealized Gains,

Stock Sales & Capital Gains Tax (continued)

content coming soon.

Also subscribe to my Youtube Channel. I have over 20 million views but a measly 20 thousand subscribers! That is one out of wack ratio but you can help fix that by clicking here

You can help support the creation of content, tutorials & projects with a small donation via Paypal and/or by using affiliate links on Shop Pages. Also subscribing to my YouTube Channel helps a ton!

Thanks for your support!

Page 1: Overview

Page 2: Read More

Page 3: Books & Video

Page 4: Glossary of Terms

Page 5: Resources & Quotes